Quantitativo weekly

Skewness · Coskewness · Transformer pairs trading · 52-week anchors · Crypto factors

The idea

“I constantly see people rise in life who are not the smartest, sometimes not even the most diligent, but they are learning machines.” Charlie Munger.

As I mentioned in the piece “Two years of Quantitativo,” the newsletter went paid. In order to continue contributing to the broader community, I decided to share quick summaries of the recent papers I’ve read over the past few weeks. These weekly research emails will be open to all.

In my experience, implementing research papers can sometimes work, though a perfect replication often fails. Nevertheless, it always helps: the ideas contained in research articles inspire new ideas and conversations with other researchers.

Here goes the first issue.

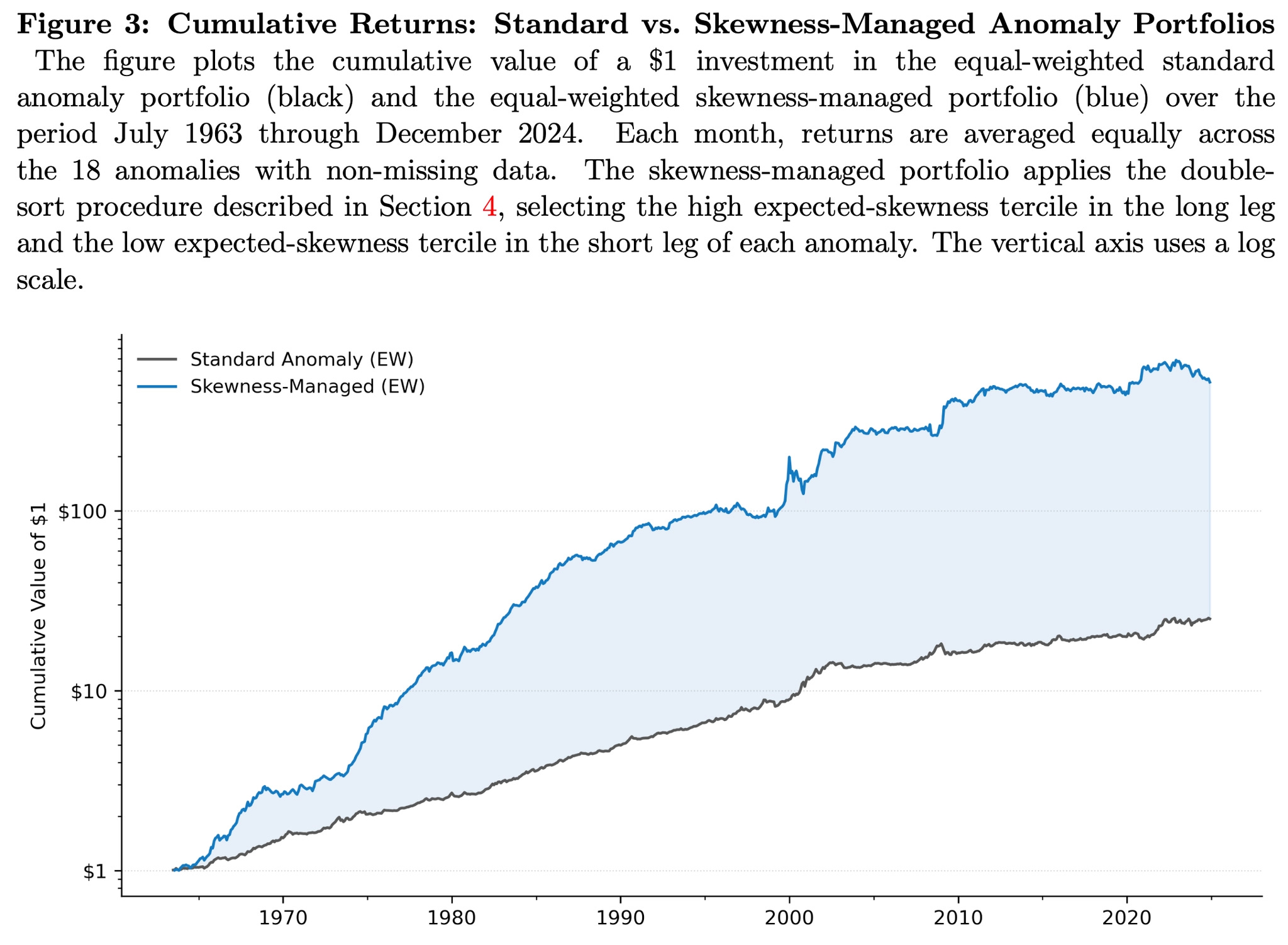

$1 grows to $530, not $22. One overlay, applied to 18 anomalies.

A new paper shows that a small cluster of extreme, positively skewed stocks drives the returns of nearly every famous anomaly, and that you can predict which stocks ahead of time.

The “skewness-managed” overlay:

Forecasts each stock’s expected skewness from simple firm characteristics (volatility, past returns, size),

Tilts the long leg toward high-skewness stocks and the short leg away from them,

Lifts average annual returns by 5.45 percentage points across 18 anomalies.

The kicker? It throws off large alphas even against factor models built from the same characteristics, and the premium balloons to 20.4% a year during recessions. Modern asset pricing models are quietly ignoring skewness.

Skewness Managed Portfolios by Gong, Lynch & Ogden (2026)

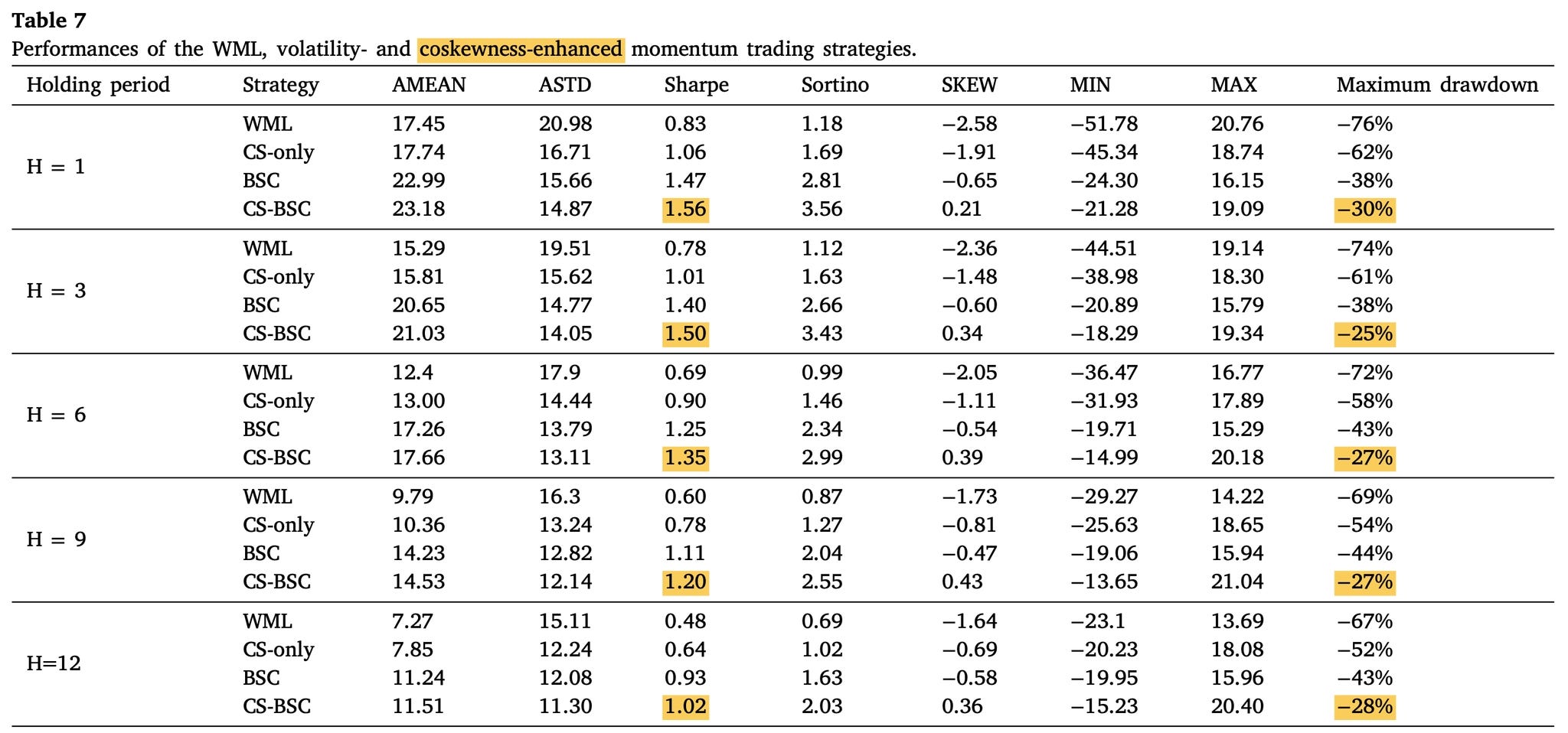

Skewness: -2.58 → +0.21. Max drawdown: -76% → -30%. Same momentum, minus the crashes.

Momentum is one of finance’s best anomalies, and one of its scariest. It crashed -91% in two months (1932) and -73% in three months (2009). The reason? Negative coskewness: winners tank exactly when volatility spikes.

This paper turns that bug into a signal:

More negative coskewness predicts higher future returns, and does so up to 9 months out, far beyond the ~1-month reach of standard momentum.

The effect lives in the tail stocks (the actual winners and losers) and is strongest in calm markets, acting as an early reversal warning.

Bolting a coskewness overlay onto volatility-managed momentum (CS-BSC) lifts the Sortino from 2.81 → 3.56, cuts max drawdown by 61% vs. baseline, and flips skewness positive.

Holds up across 3-12 month holding periods and in the UK, Germany, and France (just not Japan, which never had momentum to begin with).

The trade-off momentum traders always paid was a fat left tail. This one’s slightly right-skewed.

Coskewness and Reversal of Momentum Returns by Dong, Dai, Haque, Kot & Yamada (2022)

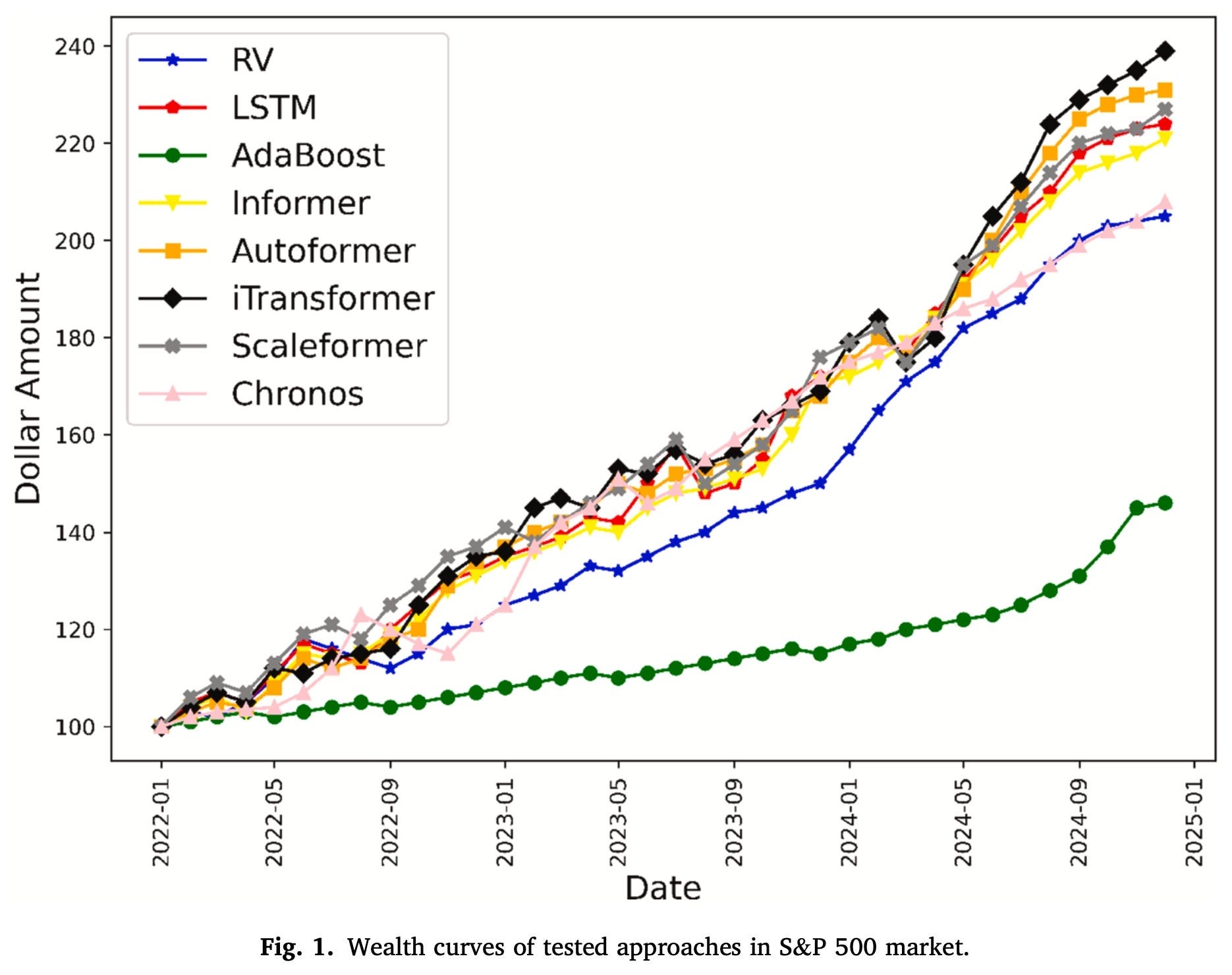

Same 60-day window. Fewer trades. 3× the Sharpe ratio.

A new paper pits the textbook Ornstein-Uhlenbeck stat-arb model against six deep time-series models on the exact same generalized pairs-trading setup, and the deep models win without trading more.

The trick is reframing pairs trading as predicting the direction of each asset’s idiosyncratic residual across the whole cross-section, not asset-by-asset mean reversion. The payoff:

iTransformer posts a 1.94 Sharpe on the S&P 500 vs 0.57 for the classic baseline; same 60-day look-back, no extra data.

On crypto, Scaleformer and iTransformer hit a ~2.2 Sharpe.

The edge survives 0.5% transaction costs (and widens as costs rise) because these models trade less: lower turnover, smaller drawdowns.

Portfolios stay market-neutral: factor betas ≈ 0, so returns come from residuals, not hidden risk premia.

The honest kicker: after multiple-testing correction, the transformers are statistically indistinguishable from each other. The win comes from the panel-prediction framing, not any single architecture.

Pairs Trading with Time-Series Deep Learning Models by Yilmaz & Sefer (2025)

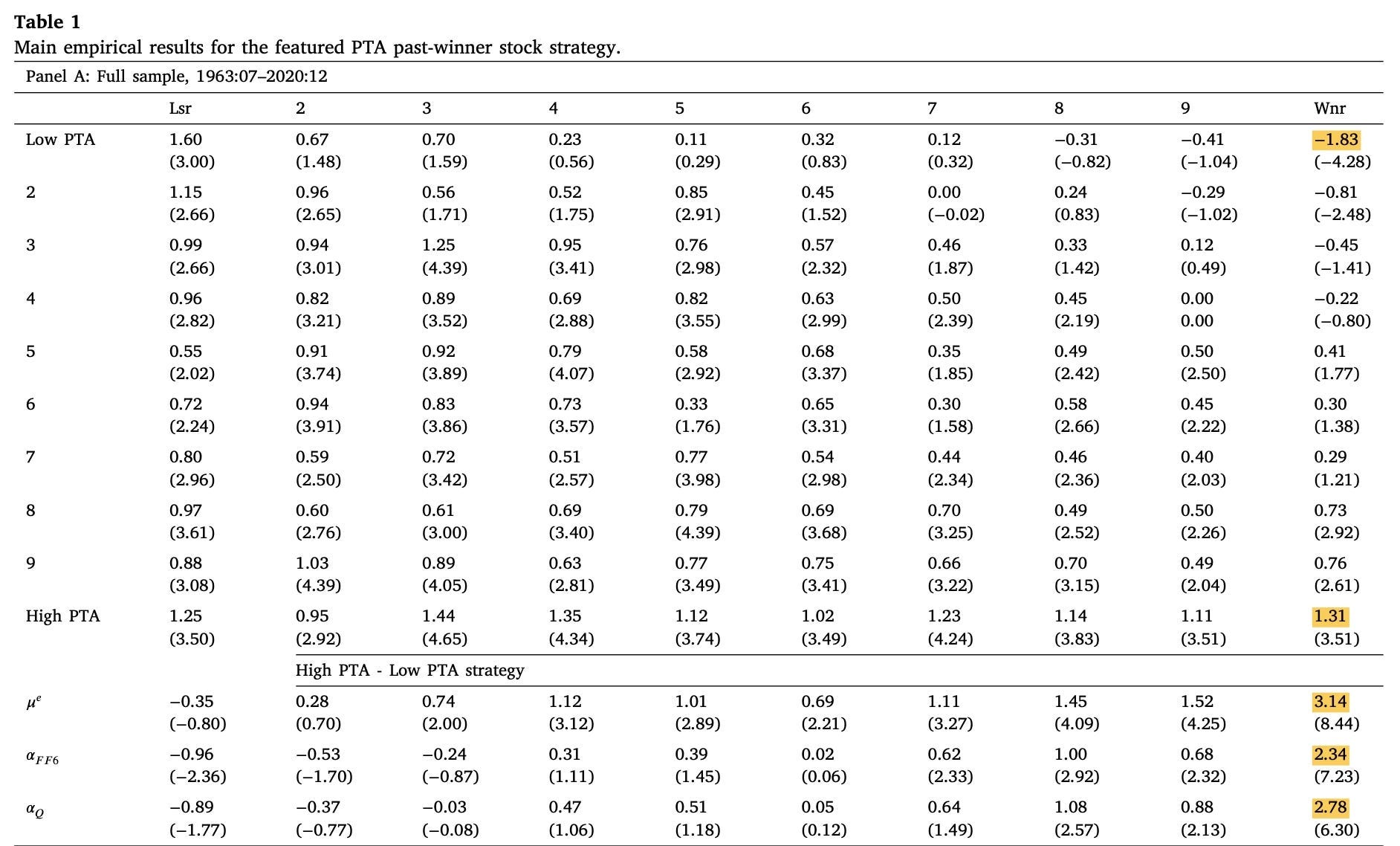

3.14% a month. 35% CAGR. A market beta of basically zero.

A new paper reveals that where a stock sits in its own 52-week range predicts a striking spread in next-month returns, for both stocks and bonds.

The signal is the Price-to-52-Week-Anchor (PTA): combining the 52-week high and the long-ignored 52-week low into one cleaner “expensiveness” measure. It works because investors anchor: they read news pessimistically on expensive-looking stocks, optimistically on cheap-looking ones, and the bias corrects next month.

Stocks: buy high-PTA past winners, short low-PTA past winners → ~3.14%/month, FF6 alpha 2.34%, ~35% CAGR, negative market beta.

Bonds: buy bonds of high-PTA past-loser stocks, short low-PTA ones → 0.72%/month, alphas >1.2%.

Strongest in high-sentiment periods and for high-uncertainty names.

First paper to show a stock’s 52-week anchor predicts its bond returns too.

Predicting stock returns of past-winner stocks and bond returns of past-loser stocks with a stock’s 52-week price anchor by Chen, Saha, Shafaati, Stivers & Sun (2026)

A t-stat of 9.80. Zero overfitting. Crypto has fundamentals after all.

A new paper introduces the Q-7 model, the first comprehensive factor framework for digital assets, blending price data, blockchain metrics, and derivatives sentiment. The findings flip several crypto beliefs on their head:

On-chain quality is king: tokens with real network usage earn the most reliable premium (t = 9.80), and it works in every sentiment regime.

Forget momentum: crypto exhibits short-term reversal, past losers beat past winners (t = 6.19), contradicting the famous Liu-Tsyvinski-Wu result.

The size premium is fake: it’s a volatility premium in disguise; orthogonalize volatility to size and the size effect vanishes.

Funding rates are a contrarian goldmine: crowded longs predict underperformance (t = 6.74), nearly orthogonal to everything else.

The model explains 63% of per-token returns and 85% of diversified portfolio returns out of sample, with an in/out-of-sample R² gap of -0.001. Essentially zero overfitting.

Crypto Has Fundamentals: A Seven-Factor Model for Digital Asset Returns by Babayev and Aliyev (2026)

As always, I’d love to hear your thoughts. Feel free to reach out via Twitter or email if you have questions, ideas, or feedback.

Cheers!