Two years of Quantitativo

Our community hits +10,000 readers

The idea

“The inches we need are everywhere around us.”

Coach Tony D’Amato.

You know the scene. A broken coach, a silent room, three minutes before kickoff. Al Pacino’s Any Given Sunday speech still gets played in locker rooms, boardrooms, and classrooms every year. Not because it’s loud, but because it’s true. The people who actually fight for things keep coming back to it. Watch it again, even if you know every line:

This month, we celebrate two years of Quantitativo! I chose to open with Tony D’Amato’s quote and speech because the past year of writing this newsletter has felt, more than anything else, like a game of inches. Let me tell you what I mean by that.

+180 shared ideas in the last 365 days

I read papers every day. A year ago, I started sharing the ones that caught my eye: short-form on Substack (to all), and long-form at connect.quantitativo.com (to the hundreds who joined the course/community). Since then, I’ve summarized and shared more than 180 of them. A few clearly hit a nerve. Here are some that resonated the most with the community (that I haven’t yet shared a detailed implementation of):

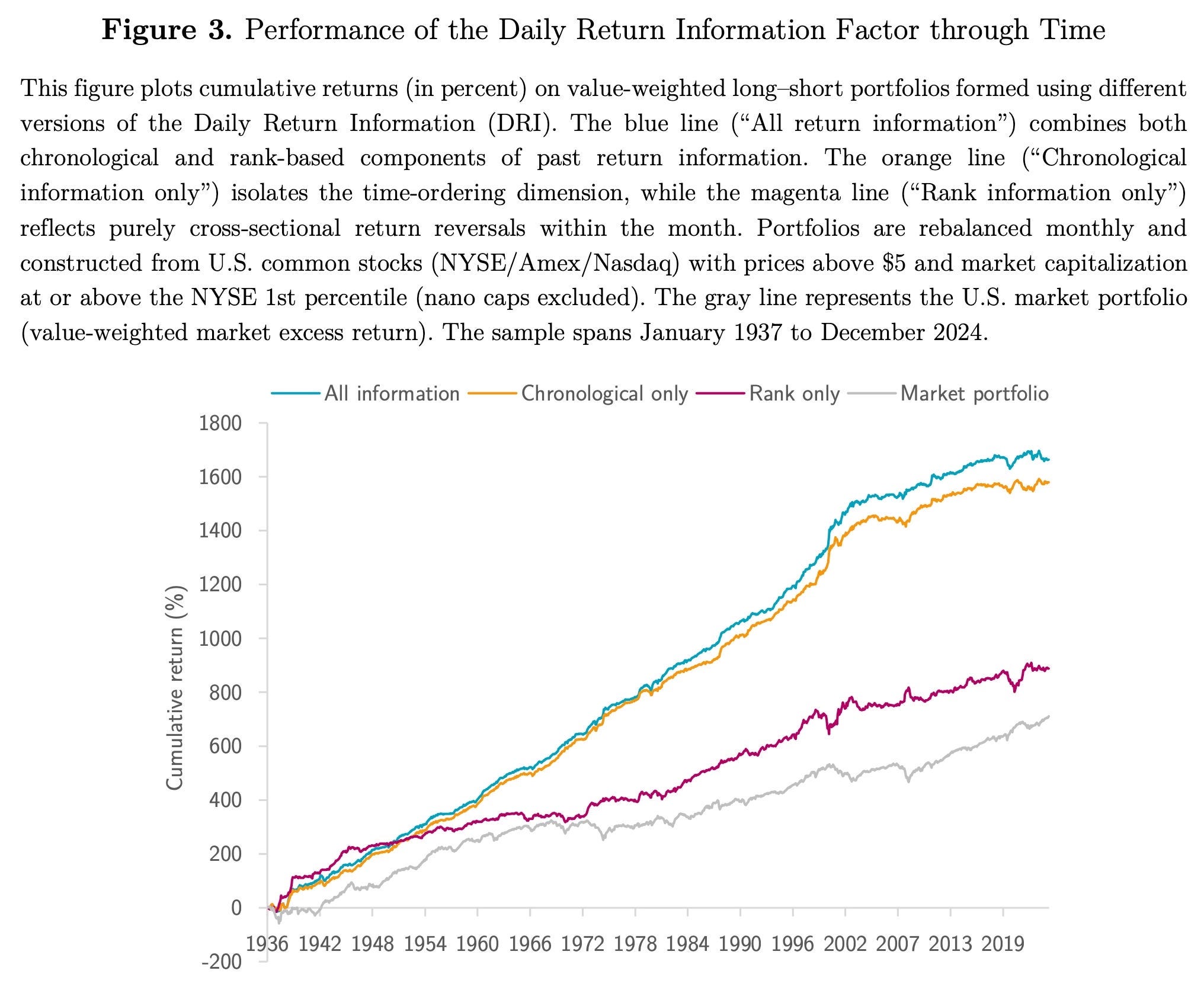

Most equity anomalies are the same trade, just badly disguised.

A new paper shows that short-term reversal, MAX, IVOL, salience, and lottery effects all come from one source: the last month of daily returns.

Instead of engineering dozens of signals, the authors let the data learn the mapping from 21 daily returns → next-month performance.

What they find:

Timing beats magnitudeWhen returns happen matters far more than how extreme they are.

A single factor (DRIF) earns ~1.6% per month, Sharpe > 1,

Subsumes most short-horizon anomalies (reversal, MAX, IVOL, tail risk),

Survives 150+ factors, multiverse tests, and modern markets.

Bottom line: The factor zoo isn’t crowded. It’s redundant. Daily returns already contain the signal: we just kept slicing them the wrong way.

Paper: A Unified Framework for Anomalies Based on Daily Returns

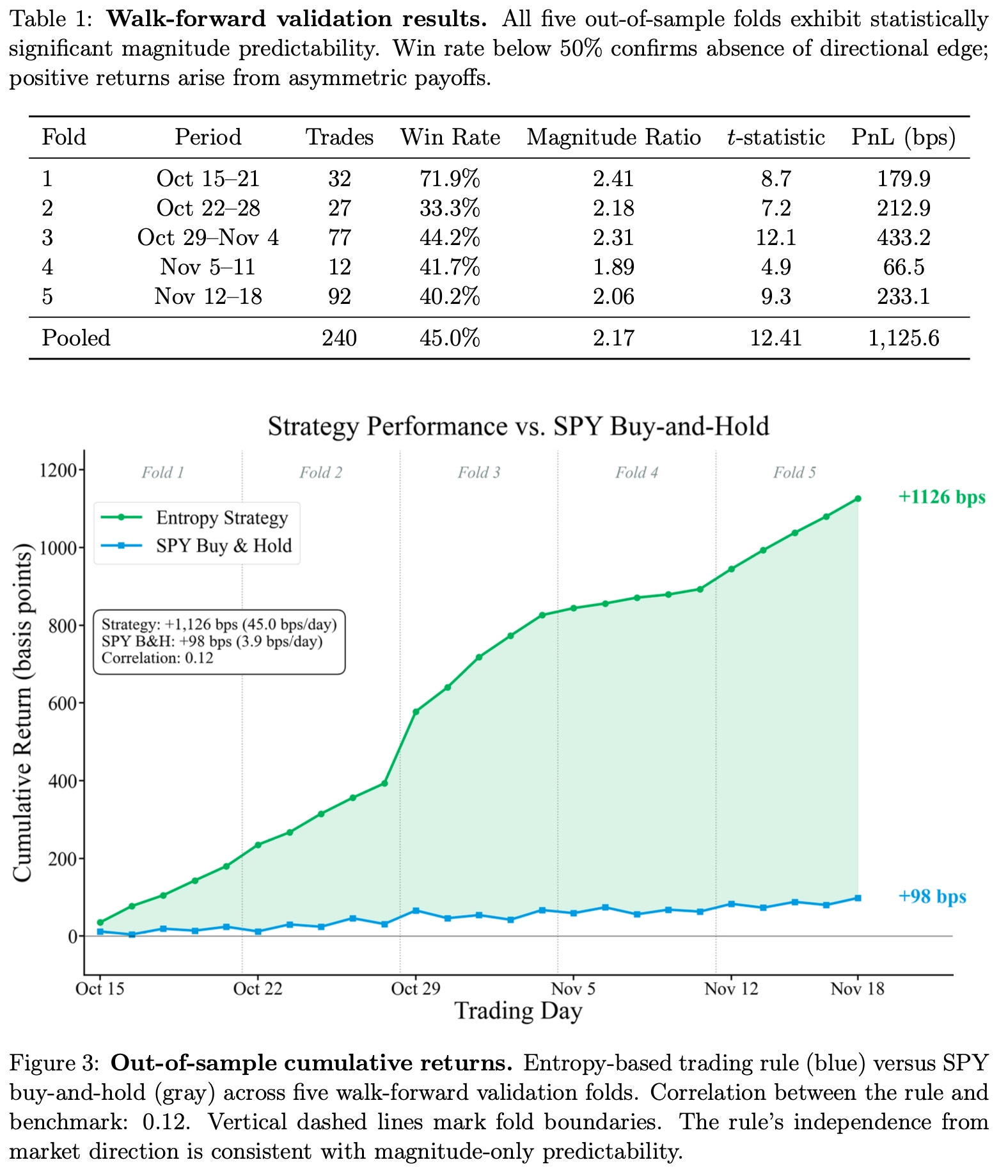

We can predict how big market moves will be without predicting direction at all.

This new paper shows that order-flow entropy from tick data forecasts future volatility, not returns.

Low entropy = structured, informed trading,

High entropy = noise trading,

Directional accuracy stays at random chance.

In SPY, conditioning on bottom-5% entropy nearly triples the next 5-minute absolute return, with zero directional edge.

The reason is deep and elegant: entropy is sign-blind. Informed buyers and sellers look identical in entropy space.

Paper: Hidden Order in Trades Predicts the Size of Price Moves

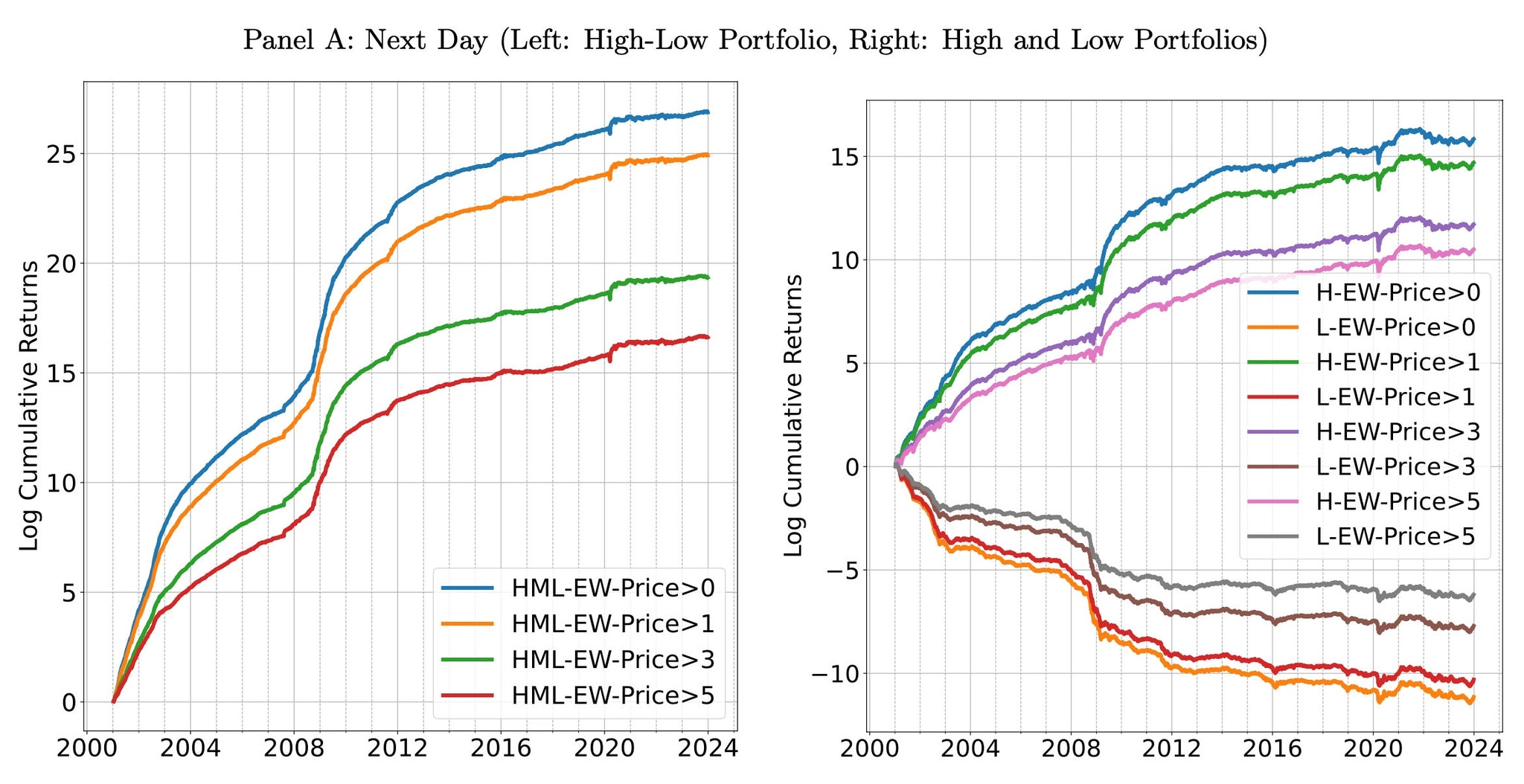

A transformer trained on stock returns beats every factor we know.

This new paper introduces StockGPT, a GPT-style model trained directly on 70M U.S. stock returns (no text, no fundamentals, just price). The result?

119% annual return, Sharpe ratio of 6.5 (daily L/S portfolio),

Still earns 69% after trading costs,

Outperforms momentum, reversals, and all 11 major stock factors,

Orthogonal to known signals.

A decoder-only transformer, trained once on data up to 2000, works 23 years later. No retraining needed.

Note: The paper doesn’t address short availability, which is a real challenge in small caps. However, even the long-only leg shows strong performance, making this paper a must-read.

Paper: StockGPT: A GenAI Model for Stock Prediction and Trading

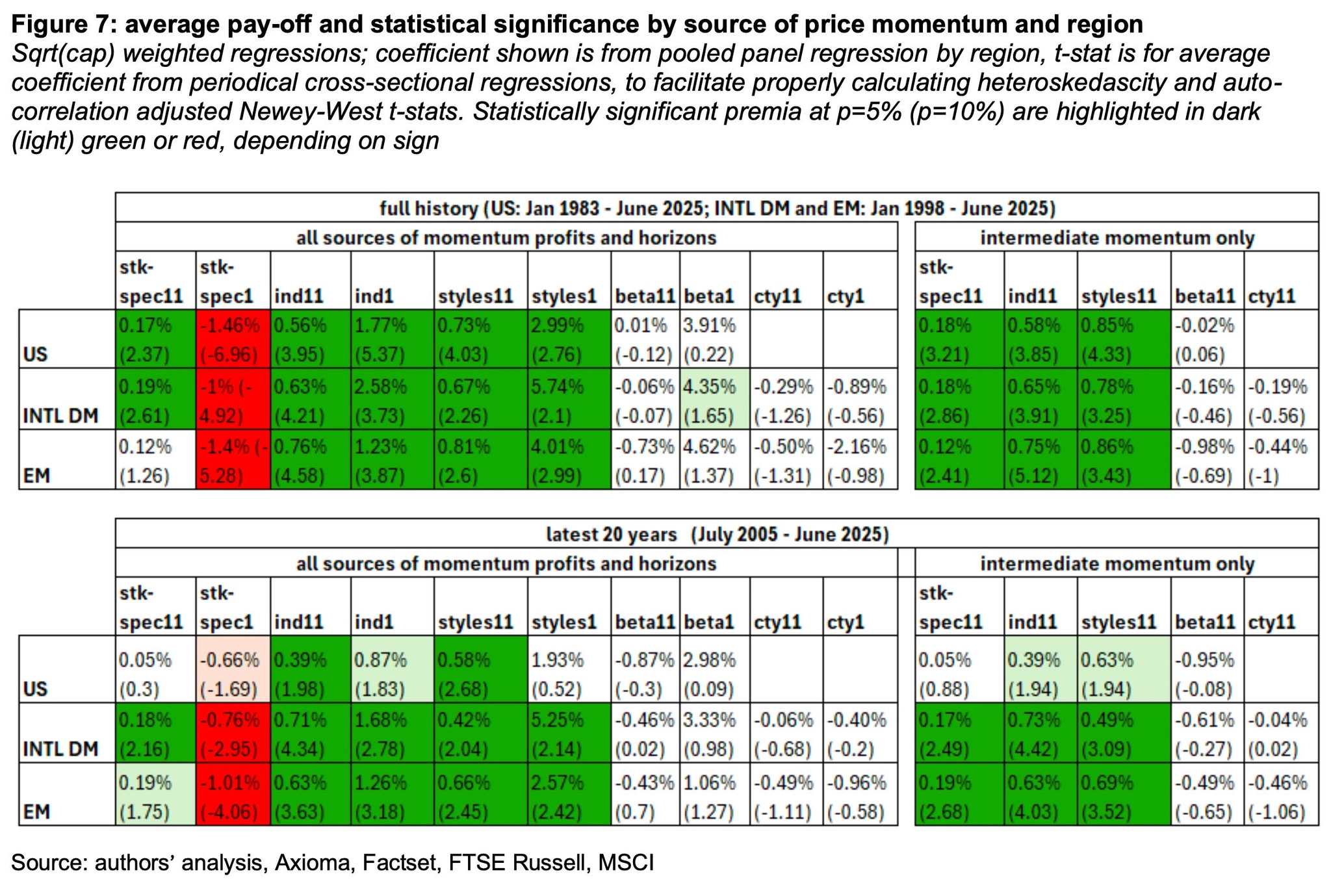

Strip momentum down to its components, and a surprising thing happens: only industry and style trends persist.

A new 2025 paper decomposes each stock’s past 12-month return into its true underlying drivers, and finds that only two sources of momentum actually persist:

Style momentum (value, quality, growth, low vol)

Industry momentum (sector & economic underreaction)

Everything else?

Stock-specific momentum reverses hard in the short run and is subsumed by industry & style in the long run.

Beta and country momentum are noise: zero premium, sometimes negative.

The shocker: What we call “price momentum” is mostly stock-specific noise (the part that causes crashes). Once you strip that out, momentum becomes far more stable, especially after low-volatility regimes.

Key takeaways:

Short-term style & industry momentum persist strongly.

Short-term stock-specific returns reverse sharply (great hedge).

Intermediate-term industry momentum is the real anomaly.

Style momentum just proxies for static factor tilts (with more turnover).

A momentum signal optimized for persistence beats classic momentum out-of-sample.

Momentum isn’t a single anomaly: it’s a hybrid of factor exposure and investor underreaction to broad economic trends.

This paper shows which trends are actually your friends.

Paper: Optimizing the Persistence of Price Momentum: Which Trends Are Your Friends?

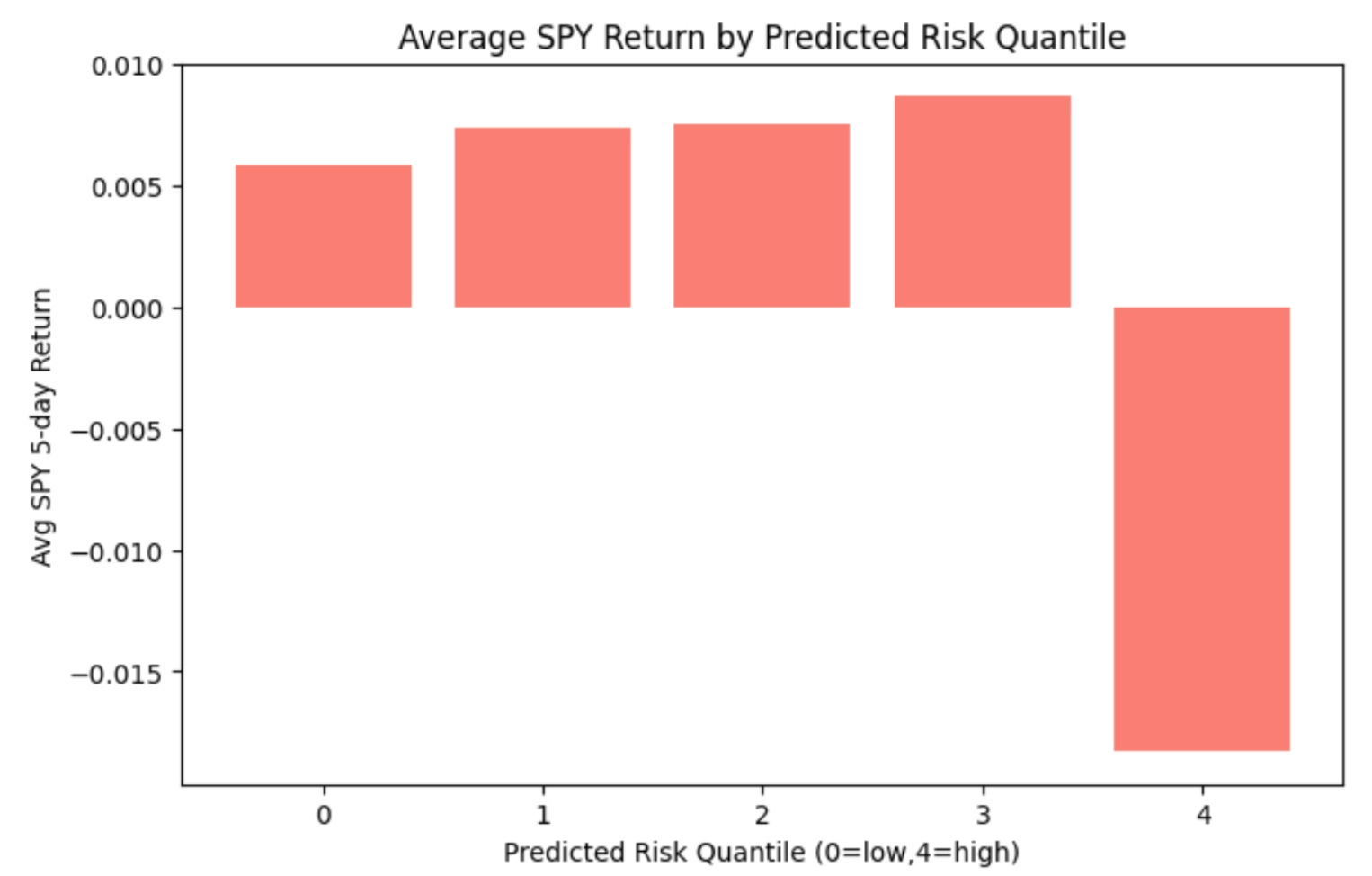

41% annual return. Sharpe 2.51. Predicting crashes before they happen.

A new paper from Oxford introduces a hybrid ML ensemble that forecasts short-horizon market risk — and trades it.

Combines neural nets + tree ensembles to predict 5-day SPY drawdowns (> 1%)

Uses cross-asset features from equities, bonds, FX, commodities, and volatility

Finds that oil, FX, and Treasury signals lead equities, warning of crashes before they hit

A simple long/short SPY strategy earns Sharpe 2.51 with beta 0.51 over 2005–2025

The insight: systematic alpha emerges from modeling risk itself (not returns) through interpretable, causal ensembles.

These are just a few. My favorites aren’t even on the list. If we tested them all, we’d find that most don’t work. A few do… and that’s the point. Along the way, we learn enough to pull ideas from different places, recombine them, and turn them into something of our own. And the learning compounds.

Let me give you an example:

The other day, I was discussing a trade idea with a friend (based on yet another paper). The gist: devising a method to identify informed/insider trading on prediction markets, and using that data to guide option trades in traditional markets. As we worked through possible approaches, I remembered something I’d read months ago about using order-flow entropy to separate informed trading from noise trading (the second paper in the list above). My friend, a veteran with two decades of experience trading options at a big Swiss bank, loved the connection: “I love it! Let’s try it out! Can you help me implement it?” I said, “Sure! Let’s do it.”

You get the point. Building a repository of ideas to pull from, recombine, and turn into something of our own is powerful. The learning compounds.

But what does this have to do with the “life is a game of inches” speech?

D’Amato’s central metaphor is that life, like football, is “a game of inches.” The difference between winning and losing, succeeding and failing, even living and dying, isn’t usually some grand decisive moment. It’s the accumulation of tiny efforts, split-second decisions, half-steps.

But here’s what makes it useful: the inches we need “are everywhere around us.” Opportunities to fight for something better are constantly available, in every moment. Most people just don’t see them or won’t claw for them.

That’s exactly what this past year has felt like. Reading every day. Testing ideas. Folding what works into the systems we trade. Most of it goes nowhere. But every now and then, an inch. And then another. The ideas we need to improve our results really are everywhere around us.

The only question is: are we willing to fight for that inch? Or are we satisfied with the inches we already have?

The best part of last year

There’s yet another important point in Al Pacino’s speech that I think of when I reflect on last year. In the end, he says the inches aren’t won alone. D’Amato tells his players to look into the eyes of the man next to them and see someone who will go that inch with them.

Last year, thanks to the newsletter, I had the opportunity to meet and work with brilliant people all over the world. Working alongside great people was the best part of Quantitativo’s second year, no doubt about that!

Isolation is death. A team, meaning any group of people genuinely committed to each other, is what makes the fight survivable and the inches winnable.

This year, we crossed the 10,000-subscriber mark, which is no small thing. But what I find more amazing about the community is not the quantity, but the quality: we have readers from places like Morgan Stanley, Goldman Sachs, Deutsche Bank, Citigroup, Millennium Management, Point72, Wellington Management, Man Group, Millburn, Trexquant, IMC Trading… to name a few. (As well as students from schools like MIT, Columbia, Cornell, UPenn/Wharton, Carnegie Mellon, Duke, NYU, Berkeley, Georgia Tech, Imperial College London, etc.)

Truly, meeting and working with brilliant people really makes my day!

What’s next

Starting with the next article, Quantitativo is becoming a paid publication.

The plan for year three is the same shape as year two, only sharper: 12 in-depth articles, plus shorter posts on ideas that catch my eye every other day. The writing has grown a lot over two years (in depth, in rigor, in implementation detail), and I plan to keep pushing in that direction.

The most rewarding part of this newsletter has been hearing from readers who’ve actually built on the work. That’s the audience I want to keep writing for.

Final thoughts

Any Given Sunday’s speech is about the dignity of relentless effort, the necessity of brotherhood, and the redemptive power of refusing to quit… even when, especially when, we’ve already lost a lot. I find it hard not to see the connection with what we do every day.

It’s where my mind goes when I think about this second year. And it’s where my mind goes when I think about year three, too.

Thank you for being part of this journey.

I’m excited for what’s ahead. The best is yet to come.

Cheers,

Carlos

Thank you for your contributions to the community! I wish you good fortune in your next phase 👍